May 1, 2026

The Markets (as of market close April 30, 2026)

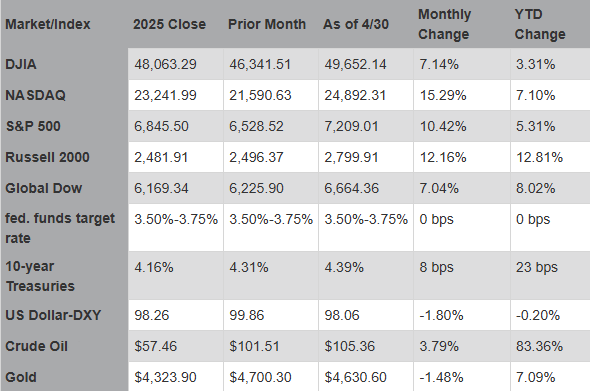

The U.S. stock market transitioned from a grim March, marked by deep-seated geopolitical anxiety, to a wave of record-breaking highs in April. U.S. stocks enjoyed their strongest month since the post-pandemic era, with the S&P 500 and the NASDAQ each reaching record highs, despite ongoing strife in the Middle East and rising inflation. After closing March at slightly above 6,500, the S&P 500 surged in April, crossing the 7,000 mark for the first time in its history. The NASDAQ also reached record levels, propelled by a 13-day winning streak, its longest in more than a decade. The Dow and the small caps of the Russell 2000 also posted notable monthly gains.

Whereas March was haunted by the risk of a full-scale war in Iran, the naval blockade of the Strait of Hormuz, and a surge in crude oil prices, April brought ceasefire negotiations and a temporary reopening of the Strait, which prompted oil prices to plummet before rising again. April's rally was also fueled by a powerful start to corporate earnings season, particularly from large tech and AI companies. Ten of the 11 market sectors ended April with gains, led by information technology, communication services, and consumer discretionary, each of which enjoyed double-digit gains. The only laggard was energy, which declined nearly 7.0%.

Price pressures accelerated in April, largely attributable to escalating oil prices. The personal consumption expenditures price index (the preferred inflation indicator of the Federal Reserve) and the Consumer Price Index each showed 12-month inflation growth of over 3.0%, well above the Federal Reserve's 2.0% target. The re-acceleration of inflation in April followed tariff-driven goods inflation from earlier in the year. Some economists noted that prices rose faster than incomes.

The labor market continued to show signs of moderate strengthening. Job growth, which had slowed considerably, rose in March. Private-sector employers added an average of about 55,000 new jobs per week in the four weeks leading up to early April, marking the fastest pace of hiring since September 2025. The unemployment rate ticked down 0.1 percentage point to 4.3% in March but was above the rate from a year earlier.

The Federal Reserve elected to hold the federal funds rate steady at 3.50%-3.75%, generally maintaining a neutral, "wait-and-see" approach, citing the need to see evidence that inflation is trending lower before considering a decrease in interest rates.

Corporate earnings season have displayed notable resilience, with the S&P 500 tracking toward its sixth straight quarter of double-digit earnings growth. According to FactSet, with about 28% of companies having reported, the earnings growth rate sits at 15.1%, outpacing the initial estimates set at the end of March. AI and technology companies have dominated earnings thus far. In addition, the net profit margin for the S&P 500 reached 13.4% this quarter, which, according to FactSet, is the highest rate since tracking began in 2009.

U.S. Treasuries saw an end to the long-running inversion that began in 2022. Longer yields are rising faster than short-term yields. The ten-year Treasury yield floated between 4.30% to 4.39%, while the yield on two-year Treasuries stayed consistently between 3.78%-3.80%. Geopolitical crude oil shock and sticky inflation, along with inaction by the Federal Reserve, has led to a repricing of Treasuries.

Crude oil prices also experienced volatility in April, largely impacted by escalating geopolitical risks and an historic diplomatic exit from OPEC+. Crude oil prices began the month at around $100 per barrel, surging past $112 per barrel, then falling to $83 per barrel before ending the month at about $105 per barrel. The primary driver of the crude oil volatility was the conflict in the Middle East in general, and the blockade of the Strait of Hormuz in particular. The retail price of regular gasoline was $4.123 per gallon on April 27, $0.162 above the price a month earlier and $0.990 higher than the price a year ago. The dollar showed resilience in April, closing the month on a bullish note despite a myriad of domestic economic factors, including a slowing labor market and persistent inflationary pressures. Gold prices vacillated throughout the month, influenced by escalating geopolitical risks and a hawkish response by the Federal Reserve.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark the performance of specific investments.

Eye on the Month Ahead

Most of the attention in May will be focused on the employment figures and inflation data for April. The Federal Open Market Committee does not meet in May.

Data sources: Economic: Based on data from U.S. Bureau of Labor Statistics (unemployment, inflation); U.S. Department of Commerce (GDP, corporate profits, retail sales, housing); S&P/Case-Shiller 20-City Composite Index (home prices); Institute for Supply Management (manufacturing/services). Performance: Based on data reported in WSJ Market Data Center (indexes); U.S. Treasury (Treasury yields); U.S. Energy Information Administration/Bloomberg.com Market Data (oil spot price, WTI, Cushing, OK); www.goldprice.org (spot gold/silver); Oanda/FX Street (currency exchange rates). News items are based on reports from multiple commonly available international news sources (i.e., wire services) and are independently verified when necessary with secondary sources such as government agencies, corporate press releases, or trade organizations. All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. Neither the information nor any opinion expressed herein constitutes a solicitation for the purchase or sale of any securities, and should not be relied on as financial advice. Forecasts are based on current conditions, subject to change, and may not come to pass. U.S. Treasury securities are guaranteed by the federal government as to the timely payment of principal and interest. The principal value of Treasury securities and other bonds fluctuates with market conditions. Bonds are subject to inflation, interest-rate, and credit risks. As interest rates rise, bond prices typically fall. A bond sold or redeemed prior to maturity may be subject to loss. Past performance is no guarantee of future results. All investing involves risk, including the potential loss of principal, and there can be no guarantee that any investing strategy will be successful.

IMPORTANT DISCLOSURES Camden National Wealth Management does not provide investment, tax, legal, or retirement advice or recommendations. The information presented here is not specific to any individual's personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable — we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Trust and investment management services are provided by Camden National Bank, a national bank with fiduciary powers. Camden National Bank is a wholly owned subsidiary of Camden National Corporation. Camden National Bank does not provide tax, accounting or legal advice. Please consult your accountant and/or attorney for tax and legal advice.

Investment solutions such as stocks, bonds and mutual funds are:

"NOT A DEPOSIT • NOT FDIC INSURED • NOT GUARANTEED BY THE BANK • NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY • MAY LOSE VALUE"