June 5, 2024

The Markets (as of market close May 31, 2024)

Inflationary data showed price pressures stabilized in April, with the Consumer Price Index and the Personal Consumption Expenditures Price Index each rising 0.3%. The CPI rose 3.4% for the 12 months ended in April (3.5% for the year ended in March), while the PCE price index was unchanged at 2.7% for the year ended in April. Growth slowed for the U.S. economy, as measured by gross domestic product, which increased 1.3% in the first quarter, following a 3.4% increase in the fourth quarter. This is the weakest rate of growth since the second quarter of 2022. Consumer spending slowed more than expected, coming in at 2.0% in the first quarter compared to 3.3% in the fourth quarter. Spending on services rose 3.9% in the first quarter, following a 3.4% increase in the previous period. Spending on goods dipped 1.9%.

Job growth slowed notably in April (see below). In addition, a slight downward revision to the February estimate and an upward revision to January resulted in employment for those two months being 22,000 lower than previously reported. Wage growth slowed on an annual basis, increasing 3.9% over the last 12 months, down from 4.1% for the 12 months ended in March. New weekly unemployment claims decreased from a year ago, while total claims paid increased (see below).

Corporate profits declined for the first time in a year, falling 0.6%. Nevertheless, about halfway through first-quarter corporate earnings season, S&P 500 companies generally outperformed expectations. About 46% of the S&P 500 companies reported actual earnings, of which 77% have reported earnings per share above estimates. Several sectors have reported favorable earnings results, including communication services, financials, industrials, and information technology. Health care has lagged.

The housing market continued to be influenced by high mortgage rates. Sales of both existing homes and new homes declined in April. Selling prices for existing homes continued to climb, while prices for new homes declined.

Industrial production was flat in April, while manufacturing output declined (see below). According to the latest survey from the S&P Global US Manufacturing Purchasing Managers' Index™, the manufacturing sector saw its first decline of the year in April. The services sector saw business accelerate but at slower pace than in March as new orders declined for the first time since October.

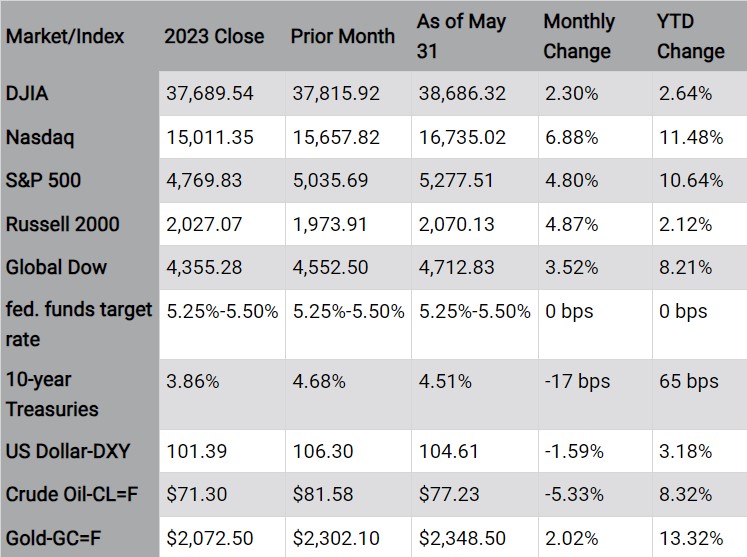

Among the market sectors in April, information technology, utilities, communication services, and real estate outperformed, while energy lagged.

Bond yields gained as bond prices declined in April. Ten-year Treasury yields generally closed the month higher. The two-year Treasury yield rose nearly 35.0 basis points to about 5.05% on the last day of April. The dollar surged against a basket of world currencies. Gold prices climbed higher. Crude oil prices dipped lower. The retail price of regular gasoline was $3.577 per gallon on May 27, $0.076 below the price a month earlier but $0.006 higher than the price a year ago.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark the performance of specific investments.

Looking ahead

The Federal Open Market Committee meets for the second straight month in June. Job growth in April was notably slower. However, inflation remained elevated. Investors will focus on how the Fed assesses this information in determining its policy stance moving forward.

Data sources: Economic: Based on data from U.S. Bureau of Labor Statistics (unemployment, inflation); U.S. Department of Commerce (GDP, corporate profits, retail sales, housing); S&P/Case-Shiller 20-City Composite Index (home prices); Institute for Supply Management (manufacturing/services). Performance: Based on data reported in WSJ Market Data Center (indexes); U.S. Treasury (Treasury yields); U.S. Energy Information Administration/Bloomberg.com Market Data (oil spot price, WTI, Cushing, OK); www.goldprice.org (spot gold/silver); Oanda/FX Street (currency exchange rates). News items are based on reports from multiple commonly available international news sources (i.e., wire services) and are independently verified when necessary with secondary sources such as government agencies, corporate press releases, or trade organizations. All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. Neither the information nor any opinion expressed herein constitutes a solicitation for the purchase or sale of any securities, and should not be relied on as financial advice. Forecasts are based on current conditions, subject to change, and may not come to pass. U.S. Treasury securities are guaranteed by the federal government as to the timely payment of principal and interest. The principal value of Treasury securities and other bonds fluctuates with market conditions. Bonds are subject to inflation, interest-rate, and credit risks. As interest rates rise, bond prices typically fall. A bond sold or redeemed prior to maturity may be subject to loss. Past performance is no guarantee of future results. All investing involves risk, including the potential loss of principal, and there can be no guarantee that any investing strategy will be successful.

IMPORTANT DISCLOSURES Camden National Wealth Management does not provide investment, tax, legal, or retirement advice or recommendations. The information presented here is not specific to any individual's personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable — we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Trust and investment management services are provided by Camden National Bank, a national bank with fiduciary powers. Camden National Bank is a wholly owned subsidiary of Camden National Corporation. Camden National Bank does not provide tax, accounting or legal advice. Please consult your accountant and/or attorney for tax and legal advice.

Investment solutions such as stocks, bonds and mutual funds are:

"NOT A DEPOSIT • NOT FDIC INSURED • NOT GUARANTEED BY THE BANK • NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY • MAY LOSE VALUE"