July 1, 2026

The Markets (second quarter through June 30, 2026)

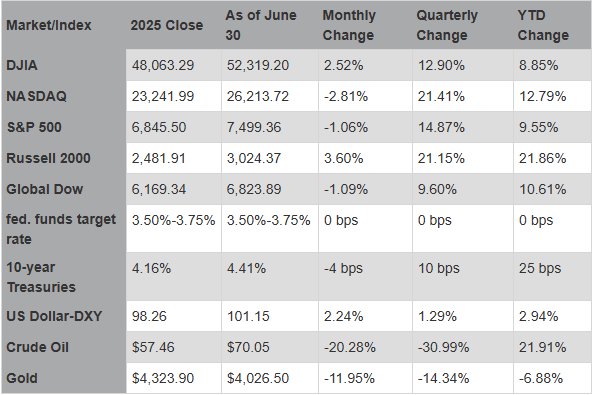

Wall Street enjoyed a solid quarter of growth during a period of time that was anything but stable. April, May, and June saw a de-escalation in a major conflict, a reaffirmation of the independence of the central bank from political pressure, strong corporate earnings, a resilient consumer, and a U.S. economy that continued to expand despite several tumultuous developments. Both the S&P 500 and the NASDAQ enjoyed their strongest quarters since 2020. The gains posted by the Dow put that index on track for its best first half in about five years and its biggest quarter since 2022. The quarter opened with investors still digesting tariff uncertainty and the ongoing U.S.-Iran conflict, which pushed energy prices higher and raised concerns about the efficacy of risk assets. There were concerns that equities were overvalued, while volatility increased as investors tried to price in the possibility of prolonged disruption to global trade and shipping routes. However, news of U.S.-Iran peace talks and a ceasefire in the Strait of Hormuz helped defuse one of the quarter's biggest concerns. The reopening of key shipping lanes and the prospect of more stable energy markets supported risk appetite, with stocks moving higher.

Information technology and communication services were the sector leaders as investor enthusiasm for AI drove much of the market. Industrials, real estate, financials, and health care also made notable strides by the end of the second quarter.

The U.S. bond market spent much of the second quarter oscillating between rising and falling yields, influenced by resilient growth, stubborn inflation, and a cautious Federal Reserve. Treasury yields drifted higher in the second quarter as energy-linked inflation coupled with fading hopes for near-term fiscal easing ultimately pushed yields up but not without periods of decline. The 10-year Treasury yield spent most of the quarter swaying within a volatile 4.0%-4.5% range. The two-year note also ebbed and flowed for much of the quarter. However, the yield curve (the 10-year yield minus the 2-year yield) shifted from a prolonged inversion into positive territory.

According to FactSet, following a blowout Q1 in which S&P 500 companies posted 28.6% earnings growth (the highest since 2021), corporate profits are expected to carry strong momentum into the second quarter. Since the start of Q2 earnings season in mid-July, analysts are projecting a year-over-year growth rate of 20.6%-21.3% for the S&P 500. Corporate America remains resilient despite market anxiety surrounding sticky inflation and a potential Federal Reserve interest rate hike in September.

The second quarter of 2026 proved to be a difficult period for gold, which endured its worst quarterly performance in 13 years. After hitting an all-time high of $5,589.38 per ounce in late January, gold prices steadily declined. Gold began Q2 at about $4,700.00 per ounce, only to slide to under $4,030.00 per ounce by the end of June, marking the first negative quarterly performance in the last 11 quarters. Typically, the tensions in the Middle East would trigger a flight to safety, boosting gold. However, surging crude oil prices stoked fears of inflation and evaporated projected interest rate cuts by the Federal Reserve, which dampened interest in non-yielding gold and other precious metals.

To describe the second quarter as a roller-coaster ride for energy markets would be an understatement. Volatility in the Middle East sent crude oil prices surging to near four-year highs in April. However, a diplomatic compromise, including the reopening of the Strait of Hormuz, led to a massive reduction in crude oil prices throughout June. April saw prices rise to a 46-month high of nearly $113.00 per barrel, more than double the price at the start of the year. Escalating crude oil prices impacted consumers at the pumps, where gasoline prices climbed to a national average of over $4.00 per gallon. In mid-May, peace talks slowed price increases, culminating in a ceasefire agreement in mid-June, which resulted in the rapid deflation of crude oil prices to about $70.00 per barrel by the end of the quarter. The retail price for regular gasoline was $3.914 per gallon on June 22, $0.561 below the price at the end of May but $0.701 more than the price a year ago. According to Freddie Mac, the 30-year fixed-rate mortgage averaged 6.49% as of June 25. That's up from 6.38% at the end of March but under the 6.77% rate from a year earlier.

Despite persistent inflation, tighter financial conditions, and geopolitical tensions, the U.S. economy showed surprising resilience. Gross domestic product held steady at an annualized rate of 2.1% during the quarter. While growth was modest, it exceeded fears of an economic contraction that prevailed throughout the end of the first quarter. The conflict in the Middle East, beginning in mid-March, had a ripple effect throughout the economy. Crude oil prices rapidly increased, inflationary pressures were felt for both products and services, and consumer spending retreated. Employment growth, which cooled in the first quarter, exceeded expectations in the second quarter, with job gains averaging 175,500 for April and May. The unemployment rate remained at 4.3% for April and May.

Inflationary pressures, which had stabilized somewhat in the first quarter, made a supply-driven return in the second quarter. Driven by rising energy prices, the Consumer Price Index spiked to an estimated annualized average of 6.0% for the quarter, while core prices hovered around 3.2%. The personal consumption expenditures price index peaked near 3.8% during the second quarter. In response, the Federal Reserve, under new leadership, maintained the federal funds target rate range but is expected to hike rates during the remainder of the year in an attempt to rein in rising prices.

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark the performance of specific investments.

Eye on the Quarter Ahead

Economic uncertainty remains elevated heading into the third quarter. While the labor market has shown strength, inflation remains "sticky," as geopolitical instability continues to be a key variable.

Data sources: Economic: Based on data from U.S. Bureau of Labor Statistics (unemployment, inflation); U.S. Department of Commerce (GDP, corporate profits, retail sales, housing); S&P/Case-Shiller 20-City Composite Index (home prices); Institute for Supply Management (manufacturing/services). Performance: Based on data reported in WSJ Market Data Center (indexes); U.S. Treasury (Treasury yields); U.S. Energy Information Administration/Bloomberg.com Market Data (oil spot price, WTI, Cushing, OK); www.goldprice.org (spot gold/silver); Oanda/FX Street (currency exchange rates). News items are based on reports from multiple commonly available international news sources (i.e., wire services) and are independently verified when necessary with secondary sources such as government agencies, corporate press releases, or trade organizations. All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. Neither the information nor any opinion expressed herein constitutes a solicitation for the purchase or sale of any securities, and should not be relied on as financial advice. Forecasts are based on current conditions, subject to change, and may not come to pass. U.S. Treasury securities are guaranteed by the federal government as to the timely payment of principal and interest. The principal value of Treasury securities and other bonds fluctuates with market conditions. Bonds are subject to inflation, interest-rate, and credit risks. As interest rates rise, bond prices typically fall. A bond sold or redeemed prior to maturity may be subject to loss. Past performance is no guarantee of future results. All investing involves risk, including the potential loss of principal, and there can be no guarantee that any investing strategy will be successful.

IMPORTANT DISCLOSURES Camden National Wealth Management does not provide investment, tax, legal, or retirement advice or recommendations. The information presented here is not specific to any individual's personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable — we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Trust and investment management services are provided by Camden National Bank, a national bank with fiduciary powers. Camden National Bank is a wholly owned subsidiary of Camden National Corporation. Camden National Bank does not provide tax, accounting or legal advice. Please consult your accountant and/or attorney for tax and legal advice.

Investment solutions such as stocks, bonds and mutual funds are:

"NOT A DEPOSIT • NOT FDIC INSURED • NOT GUARANTEED BY THE BANK • NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY • MAY LOSE VALUE"